|

Croker-Rhyne Co., Inc. |

|

Main Page |

Philosophy | Current

Recommendations |

Newsletter Archives Contact Us

|

|

|

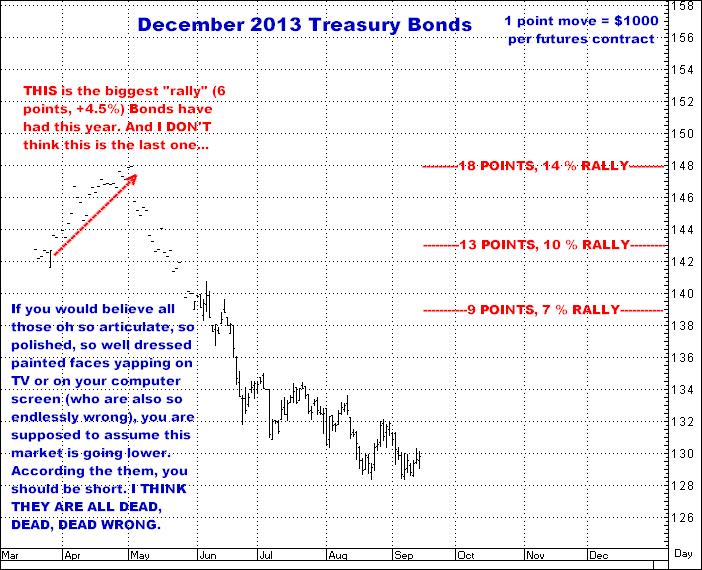

September 13, 2013 I continue to believe we are on the cusp of a 15-20 point bull move ($15,000-$20,000 per futures contract) in Treasury Bonds. I think you can take all of the almost unanimous talking head “wisdom” that is so certain rates have to go up (and bonds, therefore, go down) and throw it in the same heap with all their other perennially wrong predictions as to what any of the markets are about to do next. If you do follow all the talking heads, you are certainly aware the overwhelming majority of them are chattering about the Fed beginning to “taper”, which according to their herd of sheep “logic”, can only mean, “interest rates HAVE to go higher”, and Treasury Bonds, therefore, have to be heading lower. I think they are dead wrong, and are totally blind to the fact there is a VORACIOUS daily WORLD of demand for quality fixed income, and ESPECIALLY for U.S. Treasuries, which are universally regarded as the safest piece of paper on this planet…and that enormous demand is precisely what will send bonds higher…NOT lower. As I have repeatedly pointed out, the average daily trading volume in bonds, in just the United States, is approximately 822 BILLION DOLLARS. DAILY. And if the Fed does decide to trim their MONTHLY buying of Treasury Bonds and Mortgage Securities from $85 Billion to $75 Billion (maybe 500 million less a day), I think the idea this will somehow seriously move rates higher is just incredibly ludicrous…and just one more example of the analytic world fixating on some absurdly wrong idea supported by nothing more than the fact you can find 99 out of 100 of them agreeing on the same principle…where, the truth is, they really only believe their own “analysis” is accurate simply because they’ve heard the same “logic” a thousand times from everybody else. Believe me. Analysts are not geniuses…nor market gurus. Sure, there are some who are better than others, but they really are just guys whose job is to sound like they understand whatever area of the markets is supposedly their “specialty”. And believe me, I don’t sit here and pretend I know what’s going to happen in the markets…But I DO get it right sometimes…At any rate, I have been on the inside of this business for a long time and I will say that my impression has long been that 95% (easily) of those people you see animatedly, and even eloquently, expressing their opinions really don’t have a clue as to where ANY market is going. They have been hired to be “interesting”. They are NOT there because they have proven themselves as traders…They are in show business……Do understand, I’m not saying this because of some grudge or envy I might have for famous TV commentators…It’s simply to point out that these people, collectively, are at times the primary drivers of public opinion regarding the markets…they ARE a massive community of sheep…and if you do ever really put any faith in their supposed “savvy”, you are just asking to lose money. Sorry about that…It’s not a tirade…just one aspect of the markets I do understand (maybe)… Anyway…Think about this…The Fed HAS been spending $85 Billion on QE3 since September, 2012, supposedly representing “support” towards keeping long term interest rates low, but even though they have been steadily buying for these past 12 months, the Bond market has still fallen almost 20 points…and long term rates, basis the 30 Year Treasury, have gone from 2.5% to 3.9% in exactly that same time period. So what gives? The point is, this whole thing about the significance of the Fed spending about $4 Billion a day in a worldwide market that easily trades a $TRILLION a day has been tremendously overblown as a true bond market moving factor. Stated otherwise: If their presence had been so much of a determinant, rates would NOT have been going up. There are MANY other influences that move bond prices. I would offer this: If tomorrow morning the Fed announced they were ending QE3 TOTALLY, and tomorrow afternoon they held an auction of 30 Year Treasuries, the total bids for those Treasuries would probably be three times what the government wanted to sell…and in one fell swoop, this IGNORANT conception that rates have to go up because there won’t be enough demand for U.S. Bonds (if the Fed isn’t doing so) would be just blown out the window. Interest rates go up and down for a myriad of reasons. Bond prices do the same. Interest rates already HAVE gone up. Bond prices HAVE gone down. THIS IS WHERE YOU BUY TREASURIES. I SEE THEM 15-20 POINTS HIGHER BY NO LATER THAN SOMETIME NEXT SPRING. Maybe the following data is irrelevant but I think not… As I said, Bonds go up and down…just as stocks, commodities, and pretty much any repository of value you want to name. During the past 20 years, Treasuries have been through a series of bullish and bearish phases, often making large moves up and down inside the same calendar year…And, in fact, as can be seen from the following table, there has been some sort of fairly decent bull move, at some time during the year, in 18 of the 20 past years…See for yourself. Bull moves in December Treasury Bonds last 20 years (having taken the lowest trade for the year and then the ensuing high in that same year)

Now take a look at the current December 2013 Treasury Bond future…

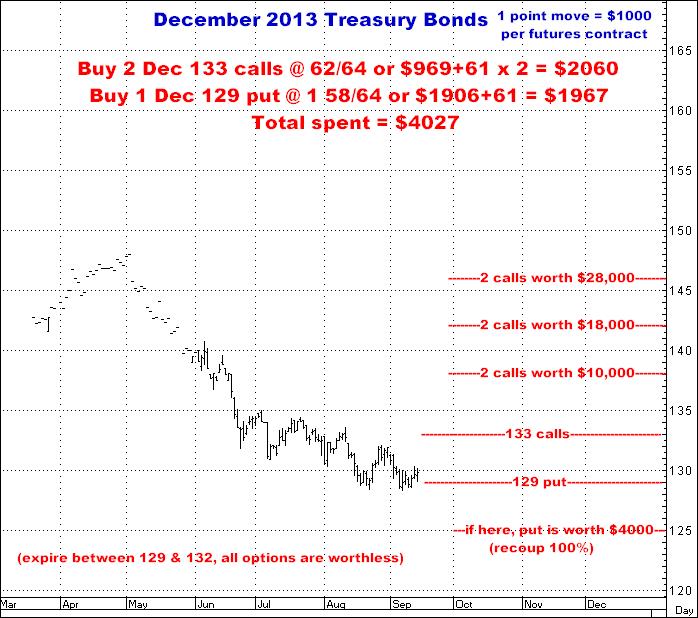

For my money, I want to be long. I AM A BUYER. I THINK THIS MARKET, THIS HIGHEST QUALITY FIXED INCOME INSTRUMENT ON THIS WHOLE PLANET, HAS NOWHERE TO GO BUT UP…and I DO THINK WE WILL SEE TREASURIES BACK AT THE 150 MARK. Buy it HERE when you CAN hear all those ever wrong TV tweety birds telling you to sell it. How many times do you have to see them have everything so absolutely backwards to EVER think you should make decisions based on what they think? UNLESS you are using them to go the other way… Here are a few ways to buy this market…

And I’ll add an attitude I haven’t expressed about a market in a long time… I trust myself more in Treasury Bonds than any other market. While I may later find myself with egg splattered all over my face, I will say it is my intention to GET LONG, and STAY LONG, TREASURY BONDS…no matter what…from here. If they go lower from here, I will buy more. If they go sideways for a while, I will buy them again. I may be dead wrong, but I personally think there is NO WAY, excepting due to some totally extraneous “black swan” event, that Bonds will NOT rally from somewhere very near current levels. Maybe this is a stupid perspective to be assuming…but, as always, I’m going to give it to you exactly the way I see it…and feel it. BUY

TREASURY BONDS AND LOOK FOR 10-15 POINTS FROM HERE, MINIMALLY, OVER THE NEXT 4-6

MONTHS. I’ve included puts I like in each market but still continue to recommend using “units” of 2 puts and 1 call whenever possible. You just can’t beat the math and the very real opportunity to get your money back when you are dead wrong…which WILL happen in this business…Also to note, all option costs shown are inclusive of all fees and commissions.

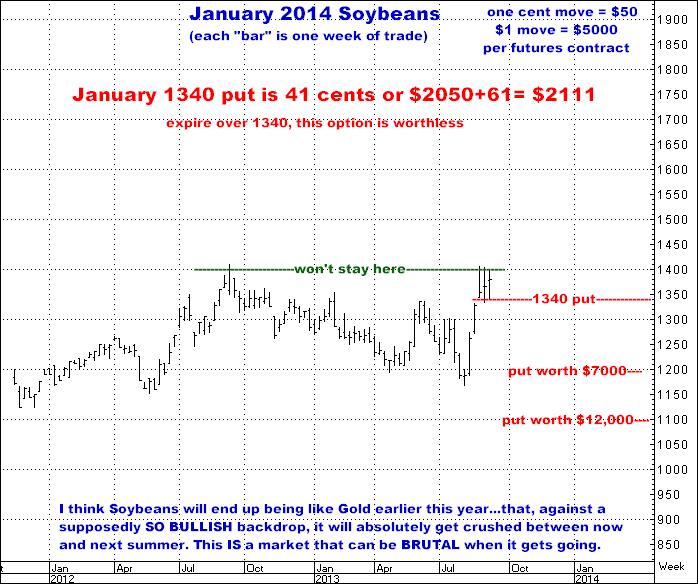

And Soybeans… Wild week. Supposedly very bullish USDA report yesterday. Weather still a factor (maybe). I think there is NO WAY this market trades sideways at $14.00. It either blows out of here with an easy 1550 target...or...it starts right back down any time now. Considering all the weather talk, AND the "bullish" report, I would view a trade back under this week's lows as the death knell for Soybeans…that the 60 cent rally off Thursday’s lows was nothing but a sucker play…I absolutely want to be short this market (especially now that the "fundamentals are undeniably bullish") but have to respect the fact Soybeans could blow off to the upside first...Therefore, sitting right here, at the highs, this is definitely a 2 and 1 situation...I firmly believe that any move on the upside will be an opportunity to establish a better short...Bottom line, big picture is: I THINK THE SOYBEAN COMPLEX COULD EASILY TRADE UNDER $10.00 BETWEEN NOW AND NEXT SUMMER…and I will be working to be sure I am there when/if it happens.

Been tough for the past 4-5 months. I think good things are about to start happening and I do think it’s time to get out your checkbook, define your risk, and go with every idea here. If just one connects, I think you can come out well ahead of the game…And if I have a few of them right, we’ve got a shot at getting into some real money…Also, obviously, if none hit, you could lose everything you put on the table. Give me a call if anything interests you here. Thanks, Bill The author of this piece currently trades for his own account and has financial interest in the following derivative products mentioned within: Corn, Wheat, Soybeans |

|