|

Croker-Rhyne Co., Inc. |

|

Main Page |

Philosophy | Current

Recommendations |

Newsletter Archives Contact Us

|

|

|

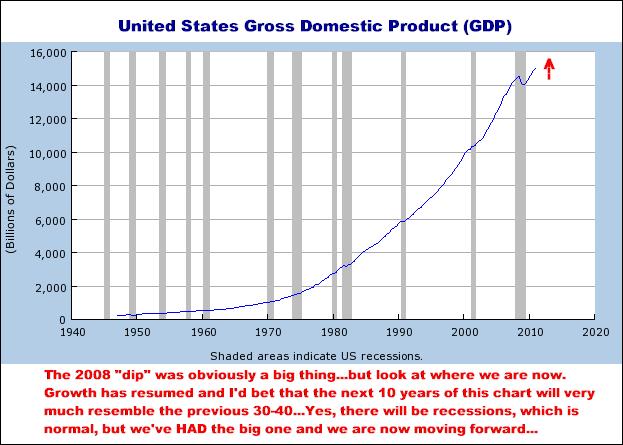

July 8, 2011 It’s been a while since I’ve written anything so I’ll just start with some random observations… The first thing that seems to be all over the place is the absurd idea (in my opinion) the USA and World economies are on the verge of going in the tank…I mean, there is a MOUNTAIN OF WORRY everywhere in the media, led by talk that the economy is not growing jobs fast enough, that 1.9% GDP is too slow for a recovery, that housing still shows no sign of a turn around, that Greece is going to collapse the world economy (???), that inflation is about to become a roaring problem, that interest rates could start heading sharply higher any day now, that the budget deficit and debt ceiling are obstacles too big to overcome…and so on. With everything I hear, you’d almost think the Dow was at 6500 again…And I absolutely disagree with all of those sentiments. If you are in the housing and construction industries, yes, these are tough times…but these two areas of the economy are just about as basic as breathing…They WILL come back…Demand has not died forever in them. And I would definitely expect to see the supposedly overwhelming supply side of the RE equation turned upside down in the next few years, to the point where there is some degree of a housing and commercial property “shortage” due to the fact that new construction has been almost nonexistent. Combine that with the pent up demand which will arise from nobody having been able to move for some three years now and I firmly believe you have the recipe for a boom in activity somewhere not too far down the road…Beyond that, I’d also add there are a number of major economic sectors…like Energy, Health Care, Technology and Agriculture, for example…that are already decidedly strong and probably going to stay that way. As for the economy not growing fast enough, I maintain that any forward progress is all we need to have. Let’s face it. We are coming out of the biggest setback since the Depression, and all the gloom and doomers who think, “Well, we have to grow at 3-4%, immediately, or we’ll never get out of this hole”, are, in my opinion, just plain wrong…And the following graph is just one example of why I believe everything is on the road to OK.

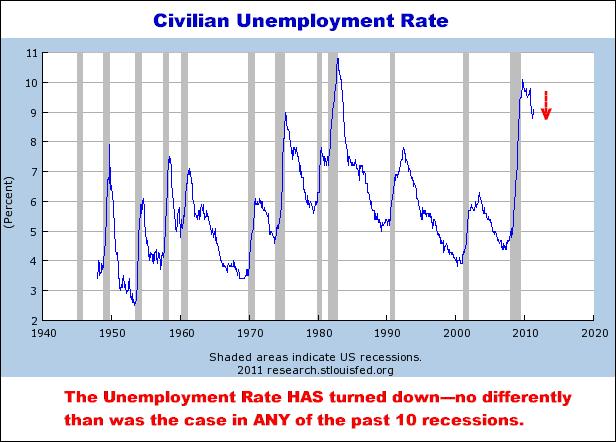

As I have noted many times, I believe the victory of Capitalism over Communism (almost a century long battle ending in 1990), combined with the still very young Technology Revolution is the perfect formula for a steadily growing world economy. There will certainly be bumps along the way, but basically the world today is all about BUSINESS…and aside from the ever upward sloping economic “inertia” implied by the chart above, I would add we also now have maybe a few billion new Asian CONSUMERS (the backbone of growth) added to the equation…which sure as hell must mean more business…for EVERYBODY. Doubt should be out. From a macro economic sense, I don’t see how the globe can be on anything other than an upswing. The debt? The deficit?...I think it is highly important to note that within a year or two, a decade of two VERY expensive wars will be behind us. While we will probably have some sort of presence in Iraq and Afghanistan, both of those dollar sucking “missions” will have been completed. Additionally, very much like the case following the 1990-91 recession, I expect to see tax revenues explode, beyond expectations, as the US economy does come roaring back, for a host of reasons…not the least of which may be that long term interest rates are going to continue heading MUCH lower, and for MUCH longer than any of the talking heads could even remotely believe. Contrary to the probably 99% of the “expert” opinion out there, I think we have semi-permanently entered an interest rate environment similar to what we had in the 1940’s and 1950’s when long term rates were in the 2.5-3.5% range…as opposed to the roughly 4.37% rate we have on the 30 Year US Treasury Bond today. To all the headline worries that still having 9.2% Unemployment “clearly indicates” the economy is improving too slowly, I just say take a good look at the next chart…From this perspective, it is blatantly obvious there is virtually zero difference between today and any of the 10 other contractions/recessions we have gone through since the late 1940’s. Employment growth ALWAYS lags economic growth as we leave a recession and this time around is no different. Jobs ARE being created…NOT LOST…and all that matters (again) is that we are headed in the right direction. We WILL reach the point where the economy is routinely producing 300,000 jobs a month…and all the political and media teeth gnashing about slow job growth just demonstrates an ignorance of economic history.

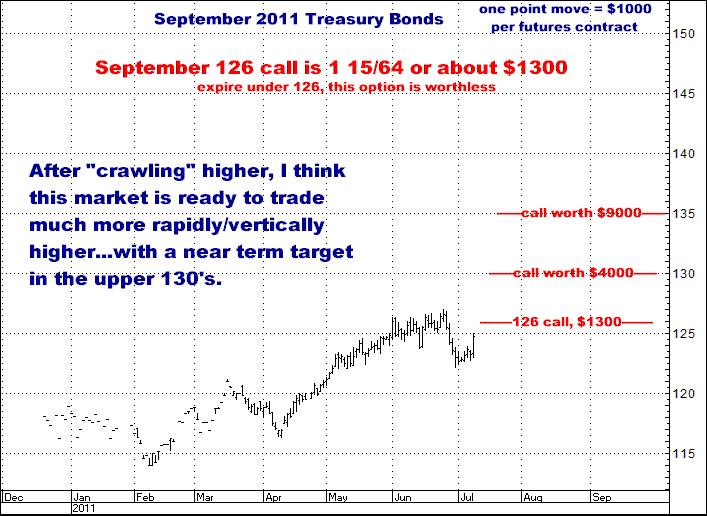

Enough cheerleading…Here are where I think there are opportunities in the markets… The “Experts” STILL hate the Bond market. (even though it has rallied as much as $13,000 per contract since February) I still believe Treasuries are going higher… And long term rates are going lower. For months now, just about every big name analyst and squawking head on planet earth has been predicting higher interest rates and lower Treasury Bond prices…and STILL are saying the same thing…and I STILL think they are dead, dead wrong. In fact, after “creeping” higher those 13 points since February, my guess is we are right at that stage where Treasuries could enter the lift-off stage, by which I mean instead of crawling higher (up 2, down 1), they just start going relatively straight up as all those hoards of forever bearish bond market sheep start throwing in the towel and jumping on (chasing) the wagon…I say this because I’ve seen it happen so many times the last 30 years…and while it may not be the case here (just because I’ve been right does not mean I will be now, I honestly believe they have a target in the high 130’s…and possibly will do so within as soon as the next 2 to 3 months. I’ve listed my reasons for being bullish the Treasury Bond market many times, so just to save time, I’ve copied the next section from a previous newsletter... If I hear one more idiot talk about the “Bond Bubble”, I will throw up. The U.S. public, led by the maturing Baby Boomers, will CONTINUE to gobble up the security of high quality fixed income instruments, inclusive of US Treasuries which are STILL the safest, most desired long term paper on the planet. During the 90’s, they all bought Stocks. Today it’s Bonds…and it will stay that way. Internationally, there are BILLIONS of dollars, every day, that HAVE TO BE INVESTED IN GOVERNMENT PAPER somewhere in the world. At 4.25 %, the 30 Year US Treasury is tremendously attractive to the SMART MONEY guys who understand they can get a great yield (relative to today’s marketplace) in an instrument that denominated in a currency, the Dollar, that is on its historical lows…meaning there is opportunity for currency appreciation in their principal as well…Even though experts galore moan and groan about “nobody will want our Bonds”, EVERY time the US Government issues new Treasuries, investors worldwide are lined up to bid on them. The 10 Year US Treasury Notes are yielding 2.76%. The Fed is nowhere near even the beginnings of an increase in rates and the 10 Year yield is NOT going higher...and more than likely (in my opinion) will be headed even lower again…There is then a MONSTER difference between that 10 year at 2.76% and the 30 Year at 4.25%...and I firmly believe that “spread” is going to narrow dramatically as the 30 Year Yield declines by at least a full 1% during the coming year... I LOOK FOR THE 30 YEAR US TREASURY BOND YIELDS TO DROP INTO THE 2.75-3.25% RANGE WHICH WOULD MEAN US TREASURY BOND FUTURES HITTING SOMEWHERE NEAR THE 150 AREA. The bottom line (super briefly) is inflation is NOT going to become a problem…and the world is NOT going to stop buying our paper…and Bond prices are going to continue going up. Bonds are NOT in a bubble. We are simply reaching the same sort of “normal” low rate environment that existed prior to the 1970’s. Back to the present…One last thought is that the end of QE2 (the government’s purchase of its own debt instruments) does NOT mean Bonds will automatically being heading lower (rates higher). To reiterate, worldwide, there are billions of dollars every day that are looking to buy quality government paper…and US Treasuries are still the highest quality interest bearing paper on the planet. Whether the Treasury is buying or not, every auction of US Government Debt is always “oversubscribed”. I CONTINUE TO RECOMMEND BUYING FUTURES AND/OR CALL OPTIONS IN TREASURY BOND FUTURES. I THINK IT ENTIRELY POSSIBLE THE RECENT SELL OFF HAS SET THE STAGE FOR A RELATIVELY STRAIGHT UP MOVE INTO THE HIGH 130’S.

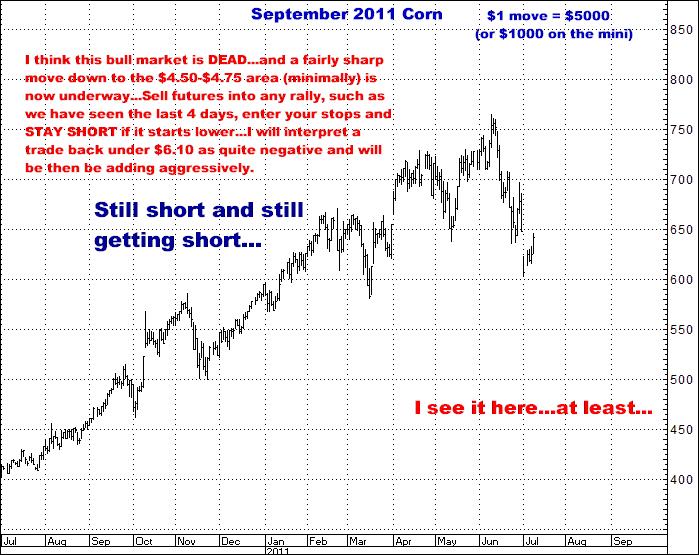

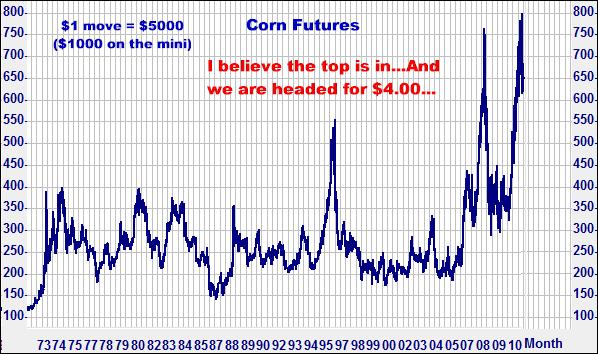

Or this can be done in the December contract…with futures or options. Still Shorting Corn Back in early June, the USDA came out with an ULTRA BULLISH supply-demand report that sent Corn roaring off into new highs (see chart below)…Not long before that, I was seeing commentary stating, “We only have a 4 day supply of corn in the pipelines! Corn is headed for $10.00!!!”…Nevertheless, the post report rally into new all time highs lasted only 26 hours, and it spite of all the enormously bullish fundamentals being touted everywhere, during the following 3 weeks, July Corn (the spot contract…where supplies are supposedly SO tight) dropped about 23% in value, or $1.85 a bushel.

THERE IS A POINT WHERE ALL OF THE “BULLISH” FUNDAMENTALS ARE ACCOUNTED FOR IN A MARKET…AND THEN YOU HAVE NO WHERE TO GO BUT DOWN. I BELIEVE THIS IS BECOMING, OR HAS BECOME, THE CASE IN VITUALLY ALL OF THE ROW CROP MARKETS. I AM STILL SHORT CORN, AND LOOKING FOR THE NEW CROP CONTRACTS, SEPTEMBER AND DECEMBER, TO END UP SOMEWHERE IN THE MID TO UPPER $4.00 RANGE.

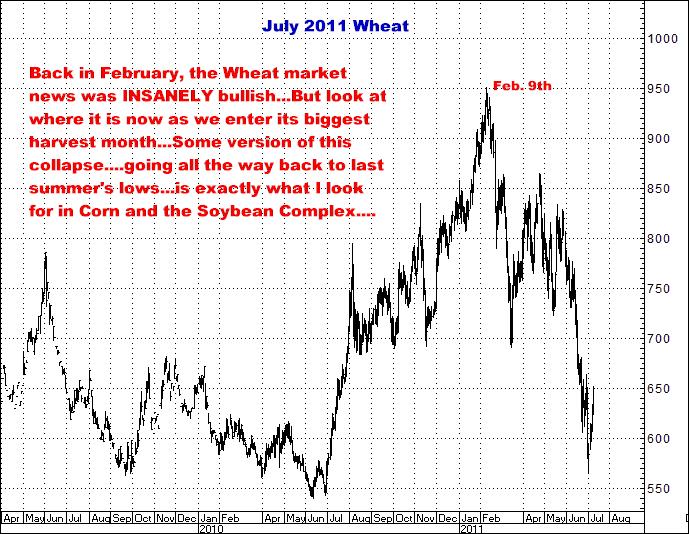

Here is a GREAT example of what I am talking about… It gets forgotten, but earlier this year, according to what was in the news, it seemed as though every Wheat producing country on the planet was losing their entire wheat crop…I mean, there was no telling (according to the analytical community) how high the Wheat market could go…but look at it now…Since all the hurrah in February, Wheat has dropped as much as 40% in price…

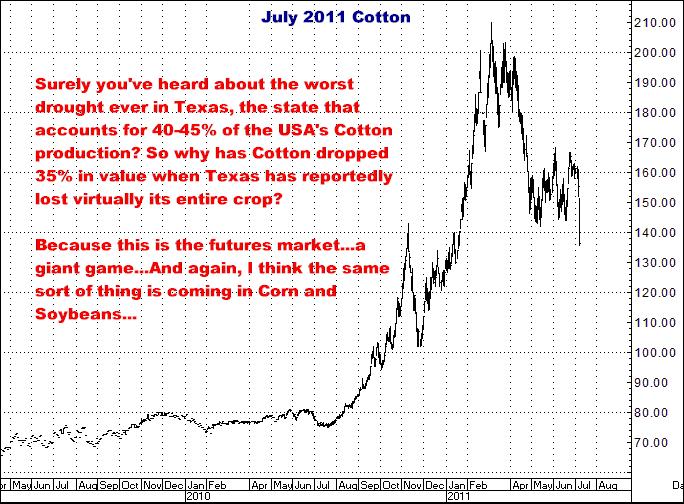

I would again point out July is the big harvest month for Wheat here in the USA…And I firmly believe Corn and the Soybean Complex will be following the same basic course for the next 2-4 months as those crops head in to their own harvest periods. Or here’s ANOTHER recent example…Back in March, with Cotton just ROARING bullish, I actually heard and read the comment several times that, “There is NO cotton left in the United States!”. I mean, how much more bullish can you get than the idea there’s not any left? That has been followed by the news, for months now, that Texas, our largest cotton producing state, was experiencing the worst drought ever, and that basically the ENTIRE cotton crop was being lost there. Thrown in with this devastation was the news that very much the same thing was happening in many parts of the Southeast…The point is, the news in Cotton has been a combination of “No cotton left” and “Drought! Drought! Drought!” for months now…but look at what this market has been doing…

I still am short the Soybean Complex. Same as in other markets, I look for a 30%-40% drop in prices. With all of the hype having been SO bullish for so long (that world demand is going to tremendously overwhelm world supply), from various conversations I have the distinct impression the average farmer has barely begun to lock in today’s high prices for the crops which are now developing in the fields…In other words, they have been, en masse, prolonging their hedge sales in expectation of even higher prices (the “I’m going to sell the hell out of it when it gets to___” syndrome)…which I believe they are not going to see…and the end result will be something like what we have already witnessed in Wheat. As harvest approaches and/or begins, and as prices weaken (and do NOT rally), more and more and more delayed farmer selling will be hitting an already unexpectedly soft market…and, as is the nature of the futures beast, there is no telling how far overdone Corn and Soybean prices will extend on the down side.

I am still buying puts in Soybean Oil…

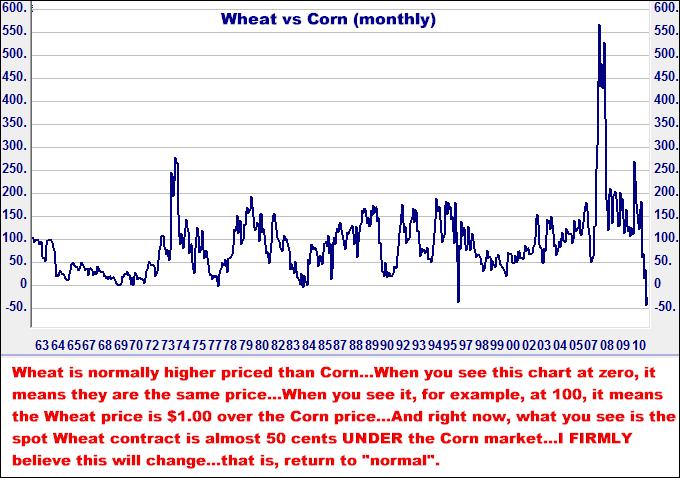

A spread trade… Buy Wheat- Sell Corn I believe futures prices are never fairly priced…that there is no true equilibrium in the markets…and prices are endlessly swinging between either being far too low or far too high. This unceasing “departure from reality” can also result in the normal price relationships between different commodities becoming severely distorted, which, by any measure you want to use, has become the case between Wheat and Corn. Without going into any detail as to why, as can be clearly seen on the following 50 year chart, Wheat is generally priced much higher than Corn…

My recommendation is to buy the Wheat-Corn spread…by which I mean, Buy the September Wheat future and simultaneously Sell the September Corn future…and then look for Wheat to increase in value relative to Corn. Your interest is NOT whether these markets are individually trading up or down, but simply how much they are changing in value relative to each other. I know the concept of spread trading (and how you either make or lose money doing so) can be confusing, so definitely give me a call if this idea interests you and I can easily explain how it works.

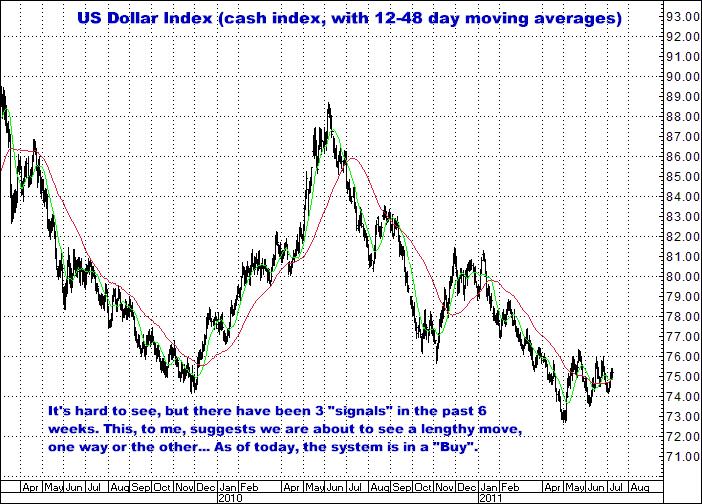

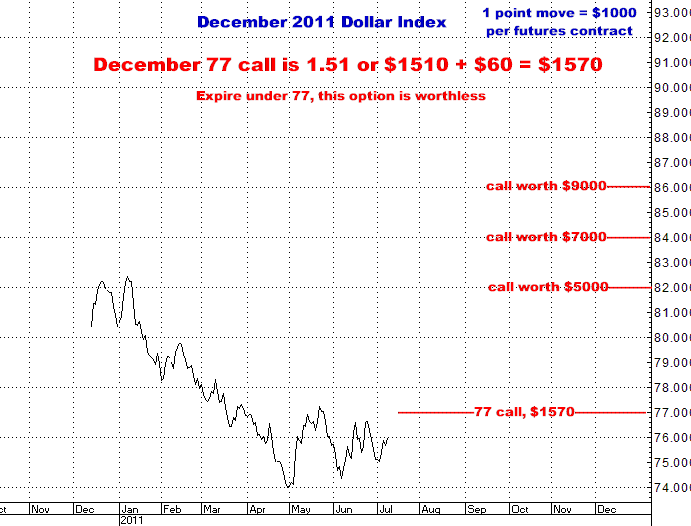

Buy the US Dollar Index If you read any financial press at all, you KNOW the whole world keeps bleating, “Sell the Dollar!”. As I point out any time I get involved with the currencies, even Allan Greenspan specifically stated (paraphrasing), “Everybody is always wrong about the currencies. No matter who, however high up the information chain they are, they DON’T know.” So if everybody is negative…and I don’t care how “logical” their opinion sounds…I want to be on the other side. I have followed the self-designed, ultra simple, moving average system shown below for over 20 years. It is not magic. It loses money when the Dollar goes sideways. It makes money whenever there is an extended move taking place…in either direction. During the past few months, as the Dollar has consolidated, it has reversed course 3 times now, which statistically speaking, now argues, I believe, that the beginning of an extended move is imminent. As of today, the system is in a Buy, and I am doing so using the September futures and call options. This has nothing to do with the system itself, but for many reasons, I do believe the US Dollar is a major long term buy…NOT a sale…and seeing it 10-15 points higher by year end would not surprise me at all.

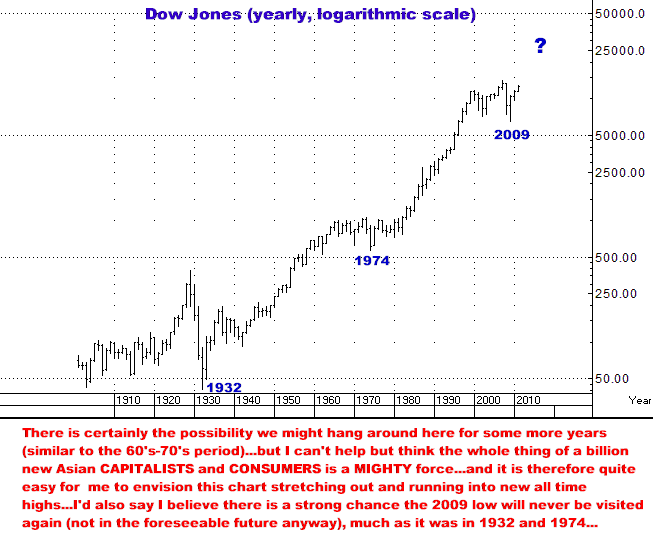

Other alternatives are using the September options and/or simply buying the futures contract with a 75-100 point ($750-$1000) stop. The Stock Market? I’m whipped. Tired of doing this letter…and still haven’t covered all the ground I’d like to…My one comment on stocks would be I still expect them to continue higher…and over time, a LOT higher…What they do short term, who knows? I would, however, again note that the majority of what I hear is worry, worry, worry…inclusive of today’s “lousy” jobs number…which inclines me to think that down days like we had today are NOT the end of the current up move. My overall perspective, though, is best described by (1) my conviction that the World and US economies are on a gigantic upswing…and (2) the chart shown below which leads me to think, as I wrote last July, that time wise, 25,000 on the Dow is not that far off.

I’d also like to address the Precious Metals (still bearish) and Cattle Complex (still bullish), but those comments will have to wait… Give me a call if anything here interests you… Thanks, Bill Rhyne

866-578-1001 |

|